![econlifelogotrademarkedwebsitelogo[1]](/wp-content/uploads/2024/05/econlifelogotrademarkedwebsitelogo1.png#100878)

Econlife Quiz: Fourth of July

July 4, 2023

How to Gobble 62 Hot Dogs

July 5, 2023

After the United States declared independence from Great Britain on July 4, 1776, we still depended on them. They had the banking system, they had the factories, they had the knowhow.

But we had Alexander Hamilton.

Economic Independence

As Secretary of the Treasury from 1789 to 1795, Alexander Hamilton supported banking, transportation, and technological innovation. He wanted factories processing what our farms and plantations grew while households and businesses easily accessed money. Only then could we truly be independent.

As we celebrate Independence Day, let’s take a look at how Hamilton’s timeless proposals related to the 18th century and now.

1. Establish Public Credit

Then

- Hamilton said a national debt is a blessing if it’s not too large. Appreciating the borrowed money that financed the Revolutionary War, he wanted those lenders to know we would pay them back. He also knew that a payback would establish the good credit we could need in the future when we again wanted to borrow. So he made sure that the debt was funded.

Below you can see that Hamilton was successful. Except for 1835 and 1836, the U.S. has always had a debt:

Now

Now

- Just like your own income determines the wise amount for you to borrow, so too does the GDP for our nation. Recently though, the debt has become an increasingly bigger proportion of the GDP. But still countries, corporations, banks, and individuals buy the U.S. bills, bonds, and notes that send borrowed money to the U.S. treasury. They believe that our public credit is dependable:

2. Create a Banking System

Then

- By establishing the First Bank of the United States, Alexander Hamilton generated the beginning of a banking system that pumped money around the U.S. economy. His goal was a network of financial intermediaries that connected savers to borrowers. He knew that a growing economy requires a network of financial institutions.

Now

- Whereas during 1791, the Bank of North America and the Bank of New York were the country’s two banks, and the First Bank of the U.S., its central bank, during 2022, there were close to 4,135 banks in the U.S. and the Federal Reserve.

Below, you can see how the number of banks has declined since 2000:

At the same time, these largest 15 financial institutions have become dominant:

3. Encourage Economic Diversity

Then

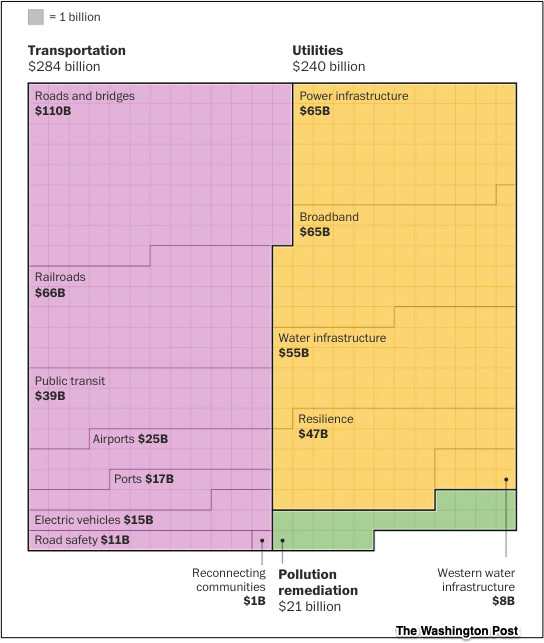

- Economic growth through diversity was the third leg of Alexander Hamilton’s plan for independence. Recognizing that the U.S. in 1790 was a farming economy, he sought tariffs to protect and subsidies to fuel a young manufacturing sector. Hamilton knew that the combination of agriculture, manufacturing, and invention could form a sturdy economic foundation. But there was another piece of the puzzle. He recognized the importance of a transportation infrastructure. He knew we needed roads, canals, and bridges to connect the country’s economic activity.

Now

- Again, 232 years later, Congress is upgrading infrastructure. Passed during November 2021, this is what they decided to fund:

Our Bottom Line: Déjà Vu

Hamilton’s goals were timeless. We still need to manage sovereign debt wisely, support a vibrant banking system, and encourage economic growth through diverse output and an up-to-date transportation infrastructure.

And finally, for the perfect summary of Hamilton’s Development Plan, do listen to the Hamilton movie musical exchange between Alexander Hamilton and Thomas Jefferson:

My sources and more: The U.S. Treasury has an ideal history of the U.S. debt until 2022. Meanwhile, if you have lots of time and patience (the sentences are impossible), to see economic independence firsthand, do go here for Hamilton’s Public Credit proposal to Congress, here for the National Bank, and here for the Report on Manufactures. Then, The Washington Post has the infrastructure story.

Please note that this post is an updated version of what we have published on past Independence Days.

{kind=link}