![econlifelogotrademarkedwebsitelogo[1]](/wp-content/uploads/2024/05/econlifelogotrademarkedwebsitelogo1.png#100878)

(Almost) All You Need To Know About Quotas

August 8, 2018

Why We Want a Starbucks Pumpkin Spice Latte

August 10, 2018

During February, we shared six facts we all should know about the future of Social Security. However, after discovering a paper from Penn/Wharton, I decided I better add another six.

But first, the basics that we always begin with:

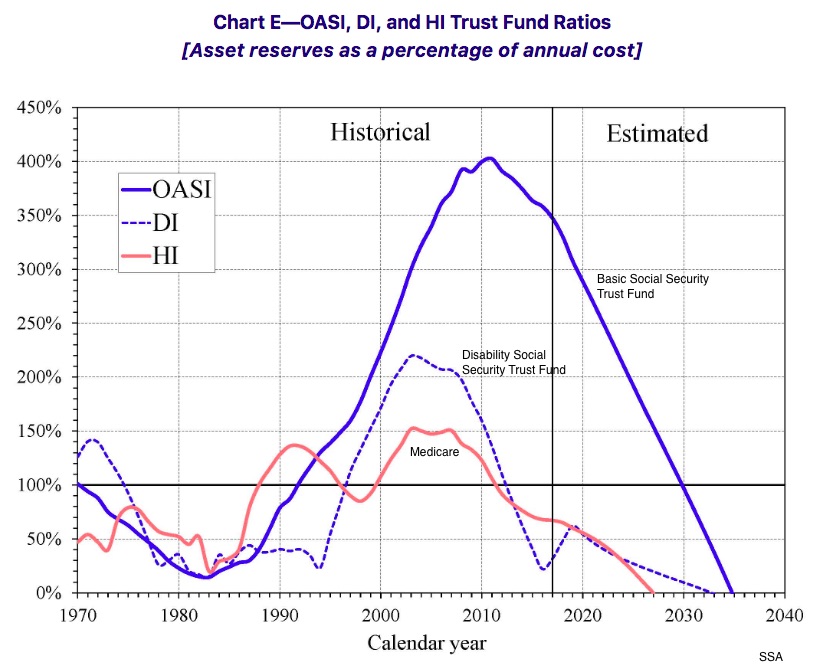

Social Security is a pay-as-you-go program. Coming from today’s workers, payroll taxes go to today’s retirees. Whenever that revenue is inadequate, money from a trust fund makes up the difference. Oversimplifying for clarity, we can just say that trust fund dollars increase when there is an annual surplus and decrease when money is withdrawn. Economists predict that the trust fund will be depleted sometime close to 2034.

Six More Facts

Problems

1.Bankruptcies among the aged have increased.

- Vastly up from 1.2, now 3.6 of every 1000 people aged 65-74 are filing for bankruptcy. They are collecting less from government programs like Social Security while traditional pension plans that cover a lifetime are no longer the norm. Instead people are deciding how much to deposit in their 401Ks. For many, it is insufficient.

People aged 65-74 did not save enough.

2. More older Americans need Social Security.

- The average monthly Social Security benefit is $1295. Social Security is 90% of the income received by 23% of married couples and 43% for individuals aged 65 and older. In the same age group, 50% of married couples and 71 % of those who are unmarried depend on their Social Security check for 50% or more of their income.

A large proportion of our aging population counts on Social Security.

3.We need more young workers.

- Now, there are 2.8 workers for every Social Security recipient. In 2035, that number will drop to 2.2. One reason is a skyrocketing elderly population that will increase from from 49 million today to more than 79 million in 2035.

With so many elderly people, the system will need more current revenue to pay full benefits.

Solutions

4.A cash infusion could help to perpetuate current benefits.

- That money could come from a higher payroll tax rate. From 12.4% on a cap of $128,400, it could increase. Alternatively, the current rate could apply to all taxable income rather than just the current capped total. Or, that cap could go up.

5.A higher eligibility age could perpetuate current benefits.

- Under current law it is increasing from 65 to 67. However, with many of us living to 80 and beyond, an age 70 threshold is a possibility.

6.The federal budget could absorb the Social Security shortfall.

- Then though, we could wind up with a debt-to-GDP ratio that exceeds 200%.

Our six extra facts focus on preserving the benefits currently that Social Security pays. On the funding side we can consider increasing the labor force, boosting taxes, and using federal funding. Meanwhile, on the benefits side, we could raise the eligibility age.

Our Bottom Line: Social Security Solvency

We have three big problems. We need relatively more workers and fewer older people. But that probably won’t happen. We need people to retire later. But many workers are unable to wait. And we need more revenue. But no one wants higher taxes.

So, when the trust fund can no longer make up the tax revenue shortfall, we will have to act. The year will probably be 2034.

Although we did not look at Medicare today, I thought you might want to get a glimpse of its trust problems also:

My sources and more: There are two ways to grasp the Social Security problem. This Penn/Wharton budget model has the facts. Or you could just do their simulation to see how you would preserve the program. Then, for specific topics, do go to WSJ, or an SSA Social Security fact sheet, For a longer look, this Social Security Primer from Congress is a possibility as is this Social Security and Medicare Trustees Report.

My sources and more: There are two ways to grasp the Social Security problem. This Penn/Wharton budget model has the facts. Or you could just do their simulation to see how you would preserve the program. Then, for specific topics, do go to WSJ, or an SSA Social Security fact sheet, For a longer look, this Social Security Primer from Congress is a possibility as is this Social Security and Medicare Trustees Report.

{kind=link}

{kind=link}

{kind=link}