![econlifelogotrademarkedwebsitelogo[1]](/wp-content/uploads/2024/05/econlifelogotrademarkedwebsitelogo1.png#100878)

An Offer Sriracha Cannot Refuse?

May 3, 2014

Should Gender Equity Include Diaper Changing Tables?

May 5, 2014

Close to one third of all households (38 million) in the US live hand-to-mouth.

Like me, perhaps you have always assumed that a hand-to-mouth (HtM) household is low income. Spending all disposable income each week, the hand-to-mouth household is unable to save. Making its plight even worse, an emergency can send it into a tailspin because there are no reserves. For an HtM household, accessing $2,000 within 30 days is tough or even impossible.

A recent paper from 3 economists, 2 from Princeton and one from NYU, disagreed. In The Wealthy Hand-to-Mouth, these scholars estimate that two-thirds of all HtM households are actually somewhat affluent. However, since their wealth is tied up in a house, life insurance, a retirement fund, maybe even a boat, it is illiquid. Converting that asset to cash would have too great an opportunity cost. As a result, as with the poor HtM (P-HtM), their disposable income can be problematic.

With age as the x-axis, here are some characteristics of the HtM household (W-HtM is blue, P-HtM, red and Non-HtM is green):

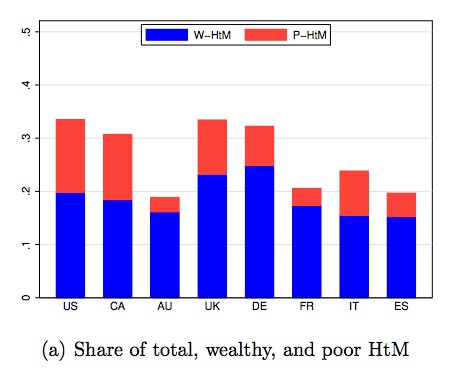

Here is the international comparison:

The US, Canada and the UK have pretty similar HtM populations while Australia, compared to the others, is the outlier because of its mandatory employer contributions to retirement accounts.

While HtM households can be investigated in countless ways, the authors of the current study had fiscal policy in mind. Reflecting a Keynesian outlook, they suggested targeting W-HtM households with a fiscal stimulus like a reduced payroll tax because they have a larger marginal propensity to consume (MPC) a proportion of any extra income. On the other hand, if you have a classical outlook, you will entirely disagree with the efficacy of the fiscal stimulus.

Here, so very excellently, in a little more than just 2 minutes, economist Justin Wolfers explains the possible fiscal connection between a stimulus and the W-HtM household.

Our bottom line? Rather like Benoit Mandelbrot’s fractal geometry, the closer you look at wealth and income, the more you see.

Sources and Resources: All facts and charts are from Brookings and The Wealthy Hand-To-Mouth.

{kind=link}

{kind=link}

{kind=link}