![econlifelogotrademarkedwebsitelogo[1]](/wp-content/uploads/2024/05/econlifelogotrademarkedwebsitelogo1.png#100878)

The Message From NFL Ticket Prices

August 10, 2014

What Refrigerators Can Tell Us About Global Markets

August 12, 2014

According to the annual Social Security Trustees Report that was submitted to the Congress on July 28th, we have some big problems. Let’s look back to 1940 and then ahead to 2088 to get a better idea of what is happening.

At 65, in 1940, Ida May Fuller got the first US monthly Social Security retirement check for $22.54. In 1941, she got $22.54 each month. In 1942, 1943, and 1944 she still got her $22.54. Until 1950, she received $22.54 a month.

You can see Ida May Fuller’s predicament. Each year, her check bought less. In 1949, she needed a monthly check for $38.32 to have the same buying power.

Realizing that beneficiaries’ purchasing power was plunging, in 1950 Congress gave Social Security its first taste of a COLA, a Cost-Of-Living-Adjustment. Since then, at first through special legislation and then automatically based on the CPI, Social Security check amounts have increased. Imagine though what happens when inflation soars as it did during the 1970s. Check totals bumped up by so much that, in 1983, a special commission recommended higher payroll taxes to fund the system and a gradual increase in the age people could receive full benefits.

So where are we now?

We have a pay-as-you-go program that just means current workers pay current beneficiaries. Those beneficiaries include:

- retired workers,

- dependents of retired workers,

- survivors of deceased workers,

- disabled workers,

- dependents of disabled workers.

In addition to the revenue from current workers’ payroll taxes, the system has several trust funds. The trust funds get more money whenever revenue exceeds spending while money is withdrawn if revenue is inadequate. As you might expect, the cash that enters the Social Security Trust Funds is invested in US government securities. Because government securities represent loans to the federal government, they pay interest and have to be sold if a Social Security Trust Fund needs more cash.

And very soon, the system will need more cash. Here are several key dates from the Trustees Report:

- 2010-2013: The Social Security program exceeded its tax and non-interest income.

- 2020: We start to deplete trust fund reserves.

- 2033 (maybe 2034 or 2035): The trust fund is empty.

- 2033-2088: Recipients get 3/4 of all promised benefits.

The reasons for the program’s financial difficulties include too many baby boomers receiving benefits, an insufficient number of workers to fund those benefits and longer life expectancy. We also have disability benefits that have skyrocketed and a disability trust fund that will be depleted during the end of 2016.

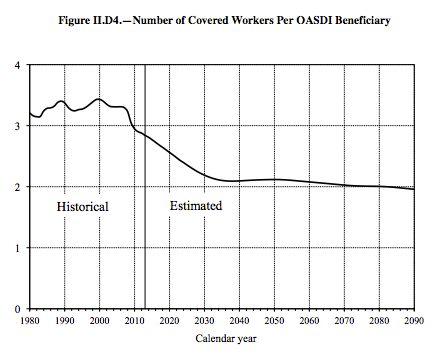

Perhaps though, these 2 graphs from the Trustees Report best summarize its problems:

Funding:

From: 2014 Social Security Trustees Report

Beneficiary Worker Ratios:

From: 2014 Social Security Trustees Report

Our bottom line: Unless we are saved by an increase in economic growth that spikes payroll tax revenue, Social Security funding challenges will involve lowering benefits, raising taxes, increasing the eligibility age and rethinking the current incentives for the disability system (that we will look at specifically during the next several weeks).

{kind=link}

{kind=link}