![econlifelogotrademarkedwebsitelogo[1]](/wp-content/uploads/2024/05/econlifelogotrademarkedwebsitelogo1.png#100878)

The Connection Between Bedtime and Gridlock

July 10, 2018

Still More on the Mommy Penalty

July 12, 2018

Zimbabwe’s monetary crises used to create money laundering…literally.

To preserve their limited supply of worn U.S. dollars, households had to wash them:

Now though, they have a new solution.

Going Cashless

Mobile money has become increasingly popular. Wherever hyperinflation is a problem, mobile money is a remedy. It also is attractive when cash is tough to access and protect.

Do follow the “red” to see how Sub-Saharan Africa is a leader in using mobile money:

These are some of the stories…

Zimbabwe

Having experienced a record setting hyperinflation and then continuing monetary upheaval, Zimbabwe turned to the U.S. dollar for its paper currency. But there wasn’t enough. The next step? Going cashless.

During 2017, digital payments dominated Zimbabwe’s transactions with mobile money topping all other alternatives. Individuals used mobile money to pay bills and merchants used it for business expenses. You can see how mobile money fills a cash vacuum.

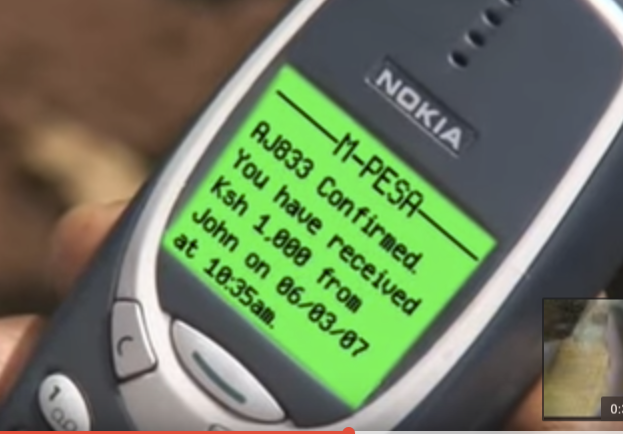

Kenya

In 2007, M-PESA came to Kenya. A banking system that was cell phone based, M-PESA just means mobile banking. (The M is for mobile and PESA means money in Swahili.) After subscribers give a deposit to a local agent, the cash becomes spendable and sendable.

With Kenya’s limited banking and ATM network, M-PESA made sense. And yet, the recent reports I’ve read could be somewhat contradictory. One says half the population uses M-PESA while another indicates that cash dominates most transactions. Although I could not confirm either statistic (and both could be accurate), we can assume there is a trend toward mobile money.

This graph displays what mobile money replaces:

Somaliland

In the breakaway republic of Somaliland, hyperinflation and the absence of banks have nudged their population toward mobile money. Called Zaad, the country’s mobile money platform is used by one quarter of their population. It does though dominate payrolls, especially since you reputedly need a wheelbarrow (and some protection) when you use Somaliland shillings.

Our Bottom Line: Financial Infrastructure

Like a heart pumping blood that carries nutrients, a banking network sends money around an economy. In the U.S., we started with the National Bank that Alexander Hamilton proposed during the 1790s. By the end of the 19th century, we had a commercial and investment banking system that moved money throughout the country.

The nations that increasingly use mobile money depend on a different kind of financial heartbeat.

My sources and more: Quartz Africa looked at the spread of mobile money as did WSJ here for Somaliland and here for developing markets. Because each article has a different perspective, for more detail, I also suggest The Economist.and the Guardian. And, I did want to note that using the term Sub-Saharan Africa is problematic since it covers over 40 diverse nations that are South of the Sahara.

As an update, this post includes sections from a previously published econlife.

{kind=link}

{kind=link}