![econlifelogotrademarkedwebsitelogo[1]](/wp-content/uploads/2024/05/econlifelogotrademarkedwebsitelogo1.png#100878)

Why Meteorite Ownership Matters

April 10, 2017

How the Power of the Market Makes Airline Passengers Happy

April 12, 2017

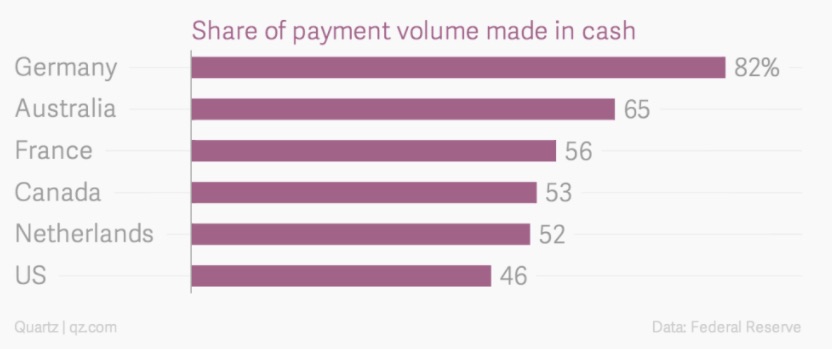

Like Mark Twain saying, “The reports of my death have been greatly exaggerated,” stories about the demise of cash are not quite accurate. Even in the U.S. where credit card and digital payment systems are increasingly popular, still we seem to like our cash.

A look at Europe, North America, and Australia reveals even more of the same trends:

Where are we going? To how we pay for goods and services.

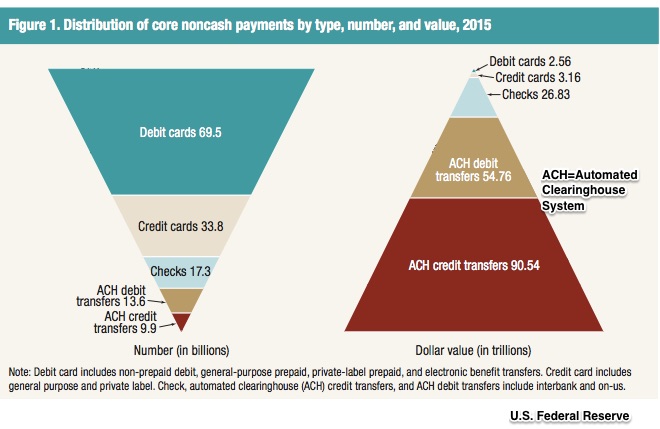

Non-Cash Payments

In the U.S., our non-cash payments are composed of debit, credit and interbank electronic transfers (through the Automated Clearinghouse System). You can see that by volume, debit cards dominate our buying behavior. However, when it comes to spending large sums of money and to our “paychecks,” then electronic transfers take over:

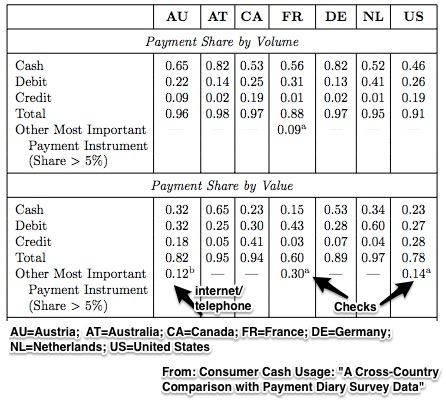

But when we look exclusively at consumer spending, still cash is pretty near the top:

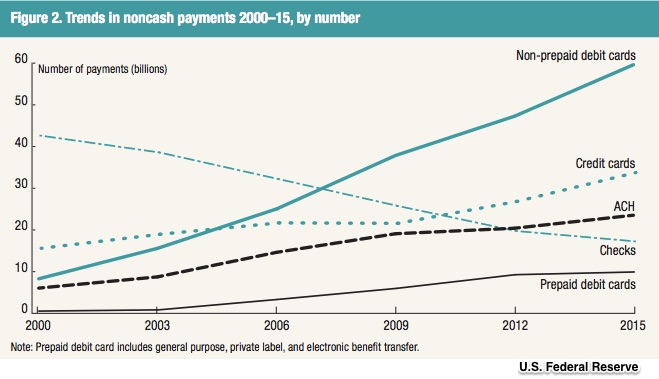

Some History

Our preferred forms of payment in the U.S. have been changing for decades. On the non-cash payment side, by volume and value, checks ruled. Now if we look at the number of transactions, cards dominate. Not shown below, we use electronic transfers to move large amounts of money:

And yet, as a percent of our GDP, at 8.6%, currency and coin are at their highest levels since the beginning of the 1950s. Furthermore, a look at the Fed’s M1 data indicates that currency is its largest component–more than demand deposits.

Our Bottom Line: Monetary Oversight

In their quest to fuel economic growth, maintain stable prices, and minimize unemployment, monetary authorities need to know the size of the money supply. And that is where the problems can start.

After all, money is any commodity that serves as a medium of exchange, a store of value and a unit of value. It can be bitcoin, a demand deposit or an electronic transfer. Cotton or paper rectangles are just one of many possible kinds of money.

So, as our dependence on cash dwindles and other forms of payment ascend, controlling the money supply will require new kinds of data collection and regulations.

My sources and more: Pretty dry today (but still rather fascinating), my data and ideas were from the U.S. Federal Reserve and the Federal Reserve Bank of Boston.

{kind=link}

{kind=link}

{kind=link}