![econlifelogotrademarkedwebsitelogo[1]](/wp-content/uploads/2024/05/econlifelogotrademarkedwebsitelogo1.png#100878)

Where We Work Less

March 22, 2026

How Grade Inflation Can Harm a Student

March 24, 2026

Reminding us again that the devastating impact of the Iran War is about so much more than the United States, The Economist looked at the hardest hit nations.

Iran War’s Impact

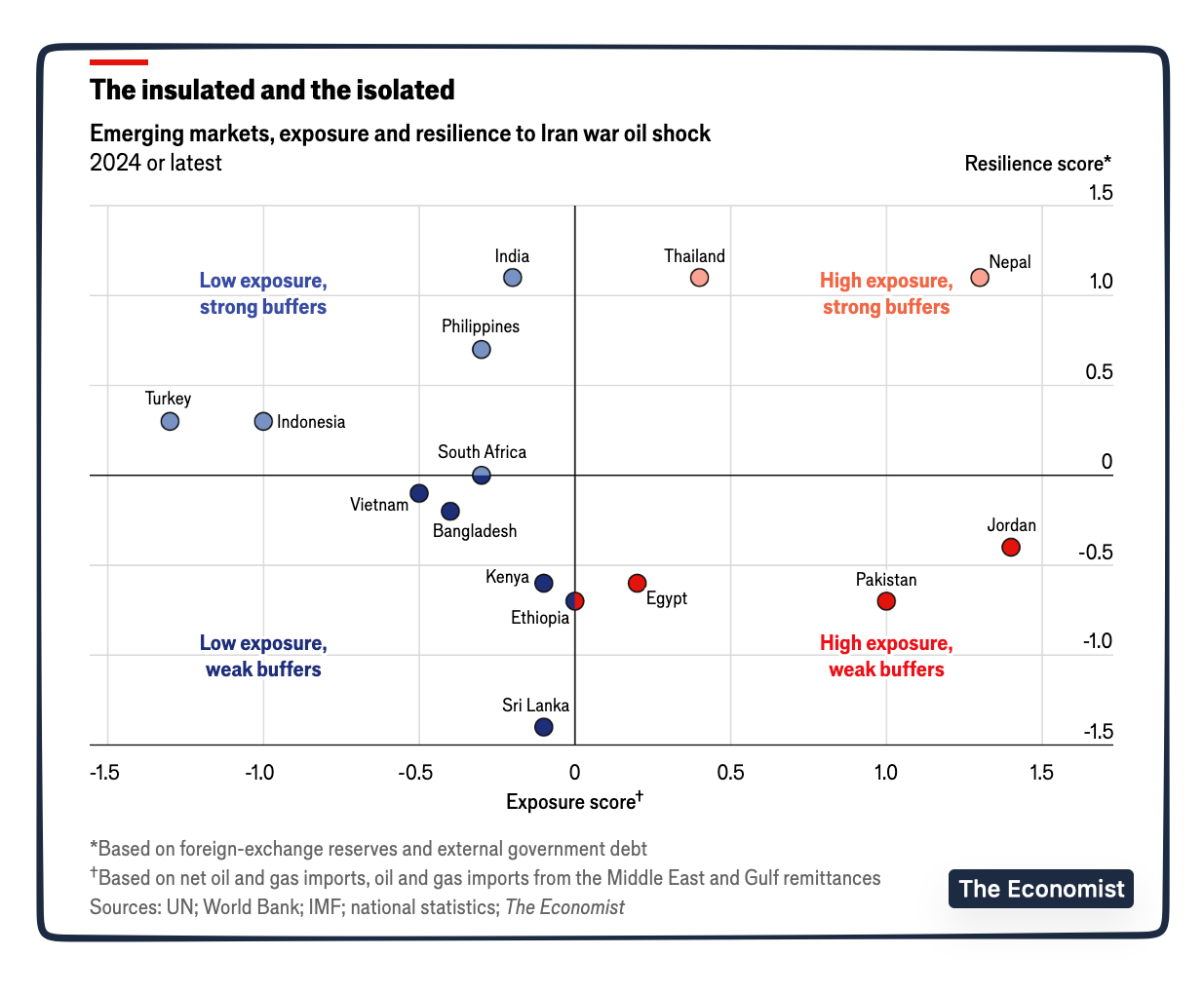

To display how the less affluent suffer the most in crises, The Economist looked at a nation’s exposure to the shock and then its ability to weather it. They first focused on oil and gas imports while the second set of criteria was financial:

The above graphic is really just about the energy price hikes that place a strain on the currencies that need to buy dollar denominated oil. From there none of the multiple possibilities is good. Basically though, we have an affordability crisis that could require more debt, more borrowing, or cuts to other imports.

But the impact varies. For Nepal, the biggest problem is the remittance Gulf workers send home that compose a whopping 8 percent of its GDP. Also they have had to ration cooking gas. Pakistan has had to close schools. India, on the other hand, gets half of its energy from the Middle East. But it has a reserve and the ability to break Middle East ties. Similarly, Thailand has a strategic reserve as its buffer.

Then, following the ripple from oil and natural gas, we could see world hunger get worse because of elevated fertilizer prices. And from there, the humanitarian cost spreads. The Philippines cut its workweek to four days for government employees. Sri Lanka and Bangladesh have begun rationing petrol. Nepal suffers from long lines because of its cooking gas shortages.

Our Bottom Line: Supply Shocks

It all adds up to the many sides of a supply shock. While most basically, we are looking at a disruption in production or distribution that shifts the supply curve to the left, there can be so much more. With the Iran War, when the Strait of Hormuz closed, 20 percent of the world’s oil and gas could no longer be shipped. But also, as targets, oil processing facilities were eliminated.

Then, following the ripple, we have production and distribution affected elsewhere through a slew of byproducts. Insurance is more expensive–if available at all. Ranging from urea to helium to sulfuric acid, a host of crucial commodities are more expensive.

So, we start with a supply shock from a war. Then we see it spread. But it’s the emerging markets and developing nations that suffer a lot from its impact.

My sources and more: Thanks to the emerging markets perspective from The Economist.

{kind=link}

{kind=link}

{kind=link}