![econlifelogotrademarkedwebsitelogo[1]](/wp-content/uploads/2024/05/econlifelogotrademarkedwebsitelogo1.png#100878)

Why a Baguette Is More Than Bread

March 5, 2026

March 2026 Friday’s e-links: A New Look At Speedy trades

March 6, 2026

Perceiving the Strait of Hormuz as a war zone, shippers are worried about crew and cargo safety, and unavailable insurance. As a result, approximately twenty percent of the world’s oil has stopped moving.

6 Facts About Crude Oil Prices

1. The situation in the Strait of Hormuz diminished supply.

However, as a Goldman Sachs podcaster points out, we need to distinguish between flow and production. For now, the flow of oil has been constrained but not a substantial amount of production.

2. Consequently prices have skyrocketed.

Close to $71.00 on February 28, yesterday Brent (the European benchmark) peaked at $85 per barrel. Correspondingly, the U.S. benchmark, WTI is also soaring:

3. Yes, spare capacity could moderate the price spikes.

However, located in the Middle East, that spare capacity is in Saudi Arabia, Kuwait, and the UAE–precisely where movement is constrained. (We should note that China could suffer the most because, in 2025, it received 13.1 million barrels a day from Saudi Arabia, the UAE, and Iraq.)

4. Middle East producers have shipping alternatives.

Pipelines can transport 4.2 mb/d (million barrels a day).

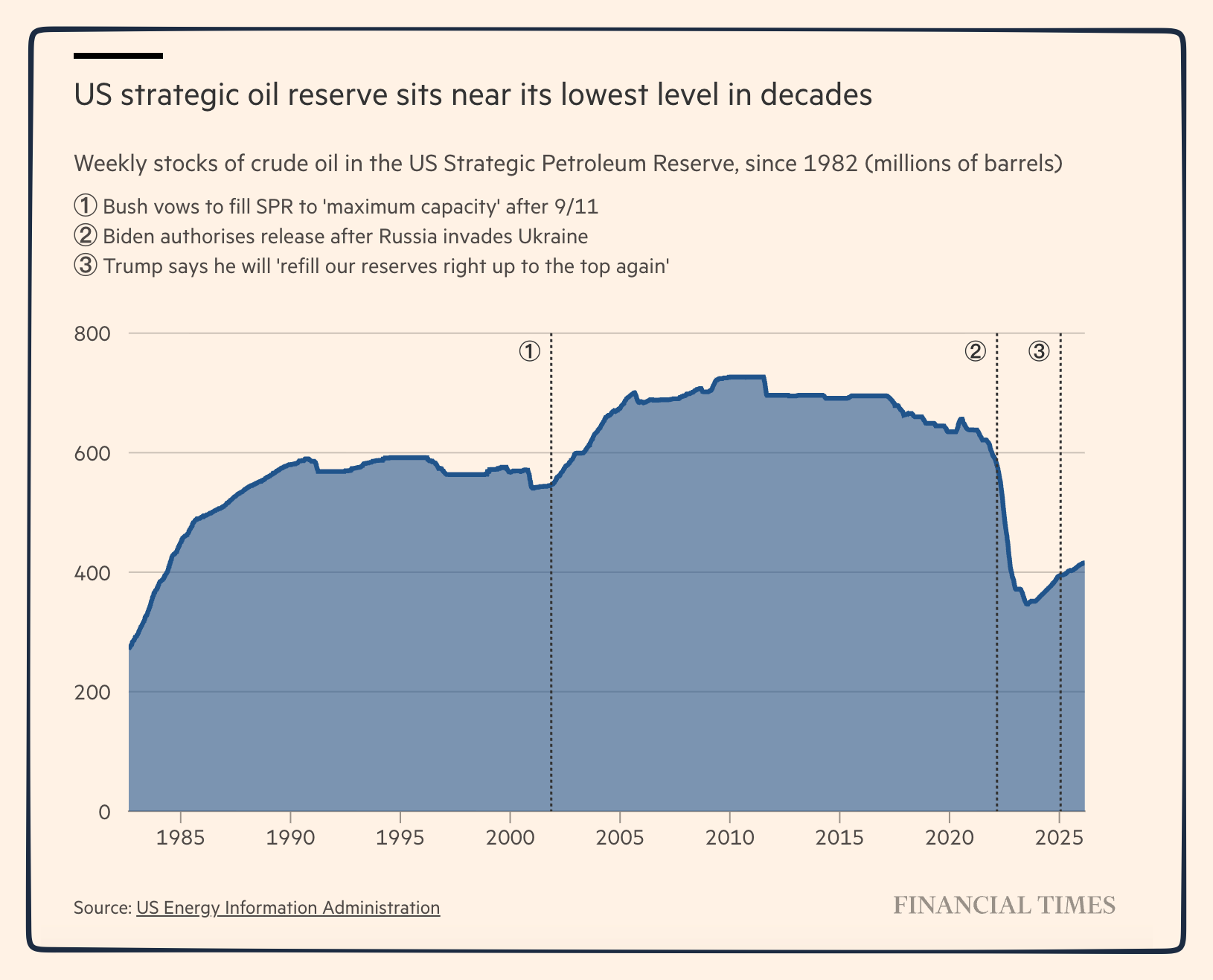

5. The U.S. does have a Strategic Petroleum Reserve.

As a backup, the SPR was partially depleted in 2022 and not refilled. We are down to 415 million barrels, close to 300 million below capacity.

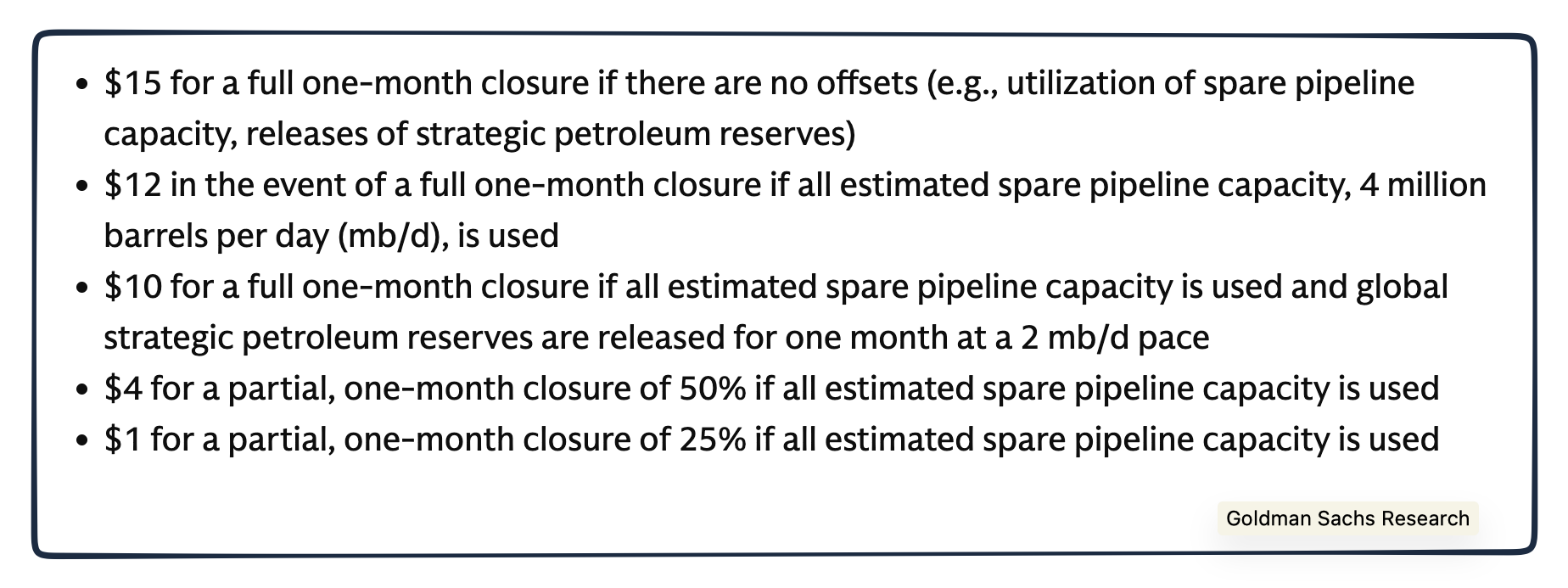

6. Ranging from $1 to $15, the increase in the price of oil depends on the closure and the offsets.

The impact of the Strait’s “closure” on the price per barrel of oil depends on a slew of variables. Assuming a one month partial or complete closure, the offsets matter:

Our Bottom Line: Feathers and Rockets

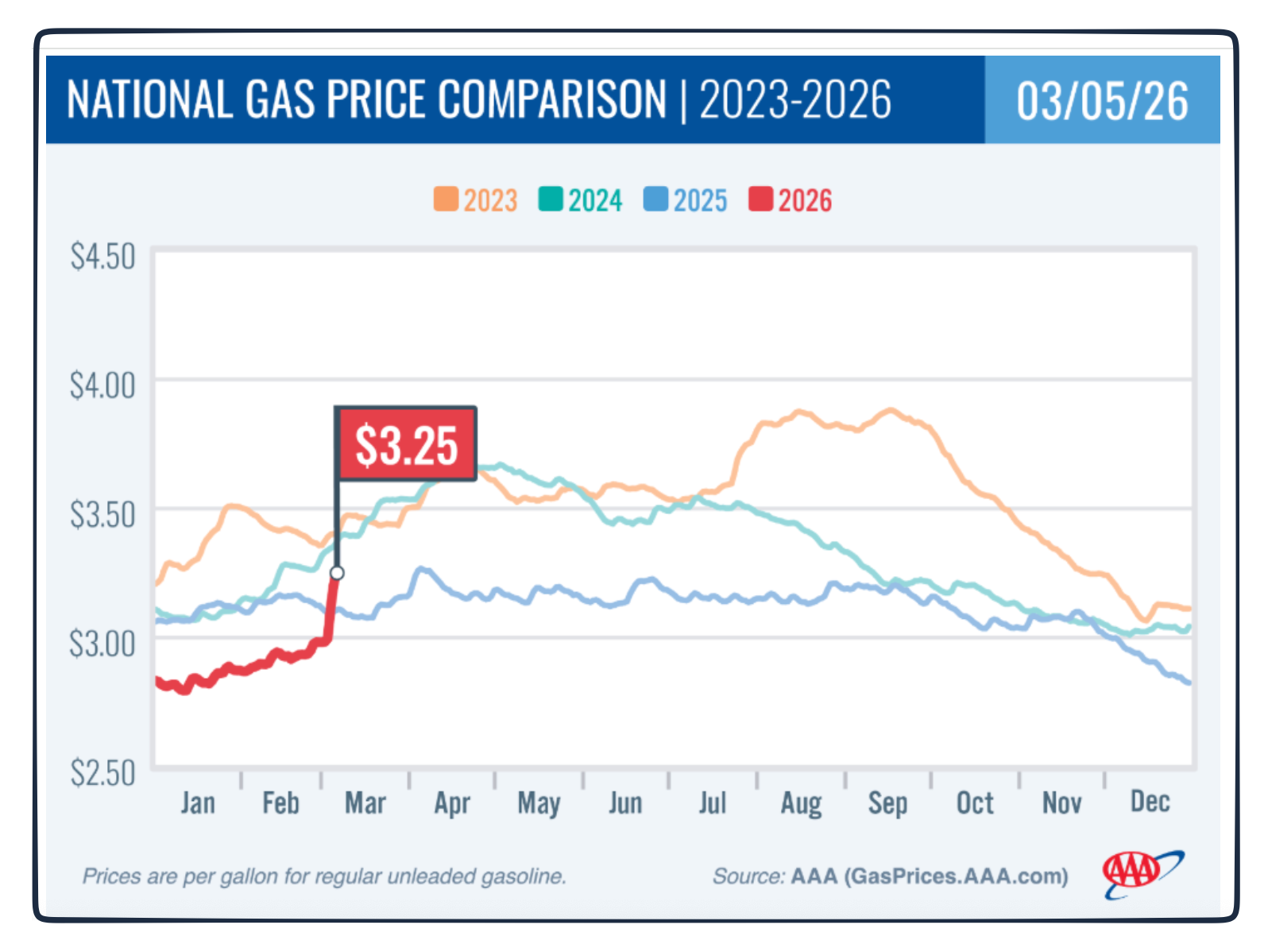

The price of gasoline is skyrocketing:

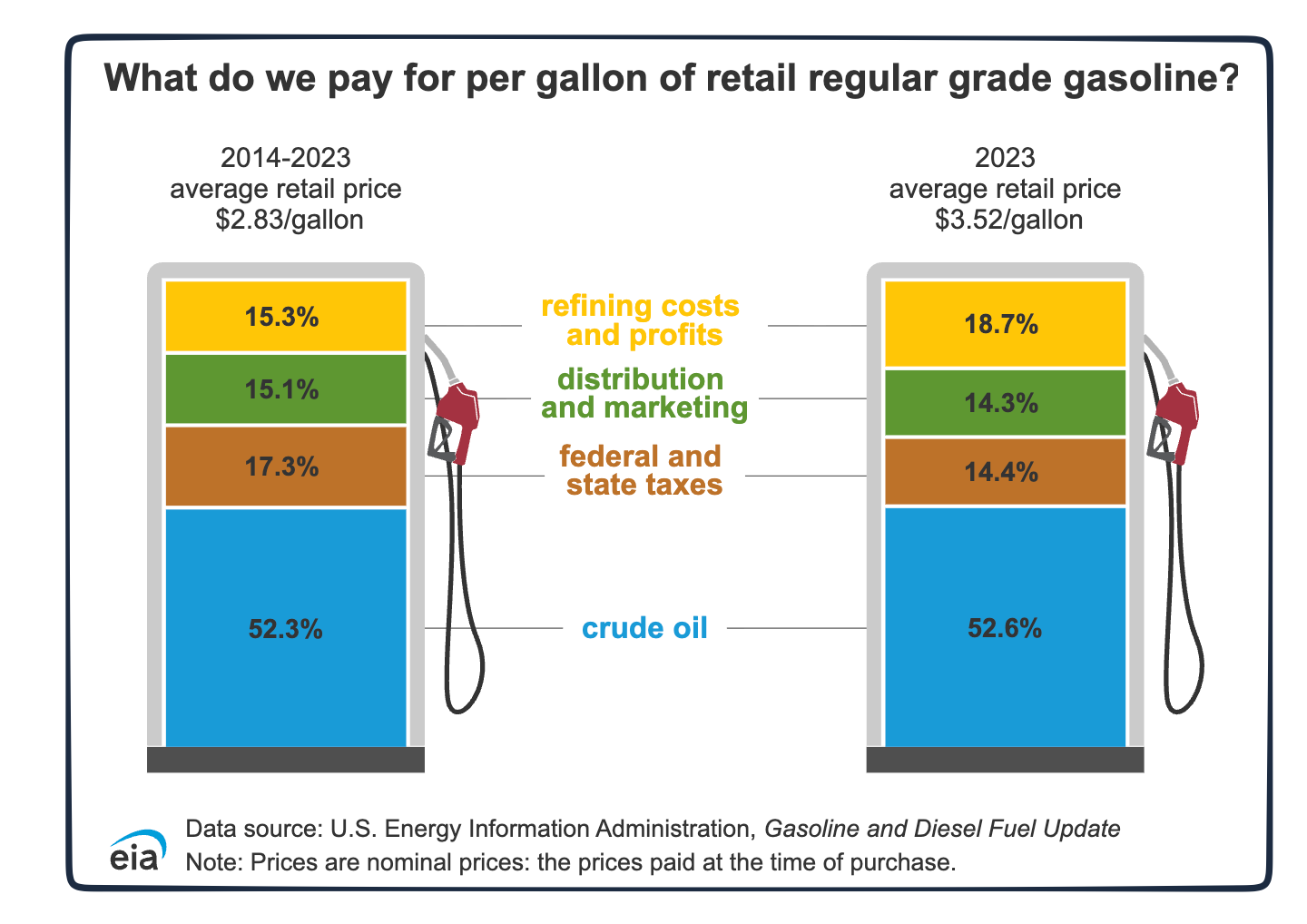

More than half of what we pay for gasoline depends on the price of crude oil:

Although the United States can be called energy independent, the price of domestic crude (WTI benchmark) relates to global markets. Consequently, all that happens in the Strait of Hormuz affects us. According to the St. Louis Federal Reserve, we can expect a $10 to 25 cents ratio; a $10 increase or decrease in crude results in a 25-cent difference at the pump. But the direction makes a difference.

Moving slowly, gas prices fall like a feather while they go up like a rocket.

My sources and more: To begin, the AAA had all the data we needed. From there, for analysis, the Goldman Sach Exchanges podcast and this Goldman article provided insight. In addition, Financial Times facts, here and here, came in handy.

{kind=link}

{kind=link}

{kind=link}